-

Best Forex Brokers

Our top-rated Forex brokers

-

NGN Trading Accounts

Save on conversion fees

-

Brokers for Beginners

Start trading here

-

Forex Demo Accounts

Learn to trade with no risk

-

ECN Brokers

Trade with Direct Market Access

-

No-Deposit Bonuses

Live trading with no deposit

-

High Leverage Brokers

Extend your buying power

-

Lowest Spreads Brokers

Tight spreads and low commissions

-

Islamic Account Brokers

Best accounts for Muslim traders

-

Market Maker Brokers

Fixed spreads & instant execution

-

MetaTrader 4 Brokers

The top MT4 brokers in Nigeria

-

MetaTrader 5 Brokers

The top MT5 brokers in Nigeria

-

TradingView Brokers

The top TradingView brokers

-

cTrader Brokers

The top cTrader brokers in Nigeria

-

Forex Trading Apps

Trade on the go from your phone

-

Copy Trading Brokers

Copy professional traders

-

All Trading Platforms

Find a platform that works for you

Last Updated On Dec 7, 2022

“The black swan in the room is the risk of the Fed being too late again, but this time in cutting rates.” – Havard Chi, Head of Research, Quarz Capital Asia.

2022 has been quite the year for the US dollar. The economic rebound from Covid, alongside Russia’s completely unnecessary invasion of one of its closest neighbours, has led to a surge in inflation unseen for over 40 years. Investors panicked, as investors do when things get weird, and the Dollar Index (DXY) has spent most of the last year in an upward cruise, wreaking havoc across the globe. But the only constant in life is change, and we are starting to see the pattern of the last year collapse.

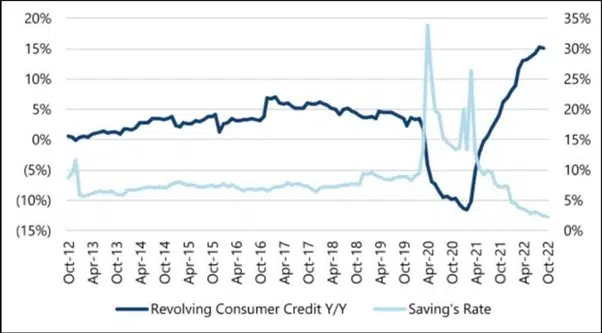

The Fed’s hawkish resilience has finally seen inflation stabilise in the US, and the USD has finally eased back from its highs, but this week’s strong economic data has spooked the markets again. Analysts fear a world in which the Fed continues to tighten the screw, even with indicators pointing to an underlying weakness in the US economy (see chart below).

Savings rates in the US are at historic lows. Credit card balances are growing +15% Y/Y. Consumers are stretched.

This fear was summed up by two of the biggest names in Wall Street on Monday, with both David Solomon of Goldman Sachs and Jamie Dimon of JP Morgan suggesting the US could enter a recession next year. But will a US recession be enough to knock the USD off its perch? That depends on what’s happening in the rest of the world.

Lifting zero COVID now could cause between 167 million and 279 million cases and between 1.3 million and 2.1 million deaths over 83 days – Airfinity Report

Let’s turn to China’s sudden retreat from its zero-Covid policy. While the Asian markets have cheered the Chinese government’s change of heart, the optimism may in short-lived. Recent modelling shows that without the current restrictions, China could be looking at “a tsunami of COVID-19 cases”, with peak demand for ICU beds at 15 times current capacity. If data modellers are aware of this possibility, the Chinese government is too. How the Chinese state plans to avoid this catastrophe is unknown. And even if they can avoid the worst-case scenario, the road back to a pre-Covid Chinese economy is going to be a long one.

Any sign that China is retreating from its reopening policy will push the USD higher – recession or not – and a Covid outbreak in China like that seen in Europe in early 2021 will be rocket fuel.

“From day one of the invasion, Russian President Vladimir Putin’s political objectives in the war have been consistently divorced from the realities on the battlefield.” – Amy Mackinnon, Foreign Policy

Finally, we come to the war in Europe, as Russia continues to bleed its military strength into the frozen ground of eastern Ukraine. While the war is expected to grind to a halt over the winter months, Putin is a master of the unexpected. Any flare-up here could push troubled European markets, already concerned about the prospect of a cold winter and the Eurozone’s own incoming recession, into a panic. The EUR/USD has climbed higher in recent weeks, but its vulnerabilities are clear.

So, what to make of this mix of unknown outcomes? We live in interesting times, and it will be a complicated winter. Whatever happens next, expect a volatile few months for the major currency pairs and the DXY more generally. I expect many traditional investors will be taking a wait-and-see approach, while speculators will be relishing the prospect of sudden rises and falls in prices.